A £100,000 pension pot may not last as long as many UK savers expect.

A £100k pension could be exhausted in just 4–5 years under a moderate lifestyle.

Rising living costs and longer retirements mean traditional expectations are no longer reliable.

- Many still assume £100k is enough

- Inflation is reducing pension value quickly

- £200k+ is becoming a safer target

Snapshot

Pension Pot Snapshot

| Pension Pot | Annual Spend | Duration | Insight |

|---|---|---|---|

| £50,000 | £25,000 | ~2 years | Very limited support |

| £100,000 | £25,000 | ~4 years | May run out quickly |

| £200,000 | £25,000 | ~8 years | More stable |

| £500,000 | £25,000 | ~20 years | Long-term support |

Note: Estimates assume moderate spending and include State Pension.

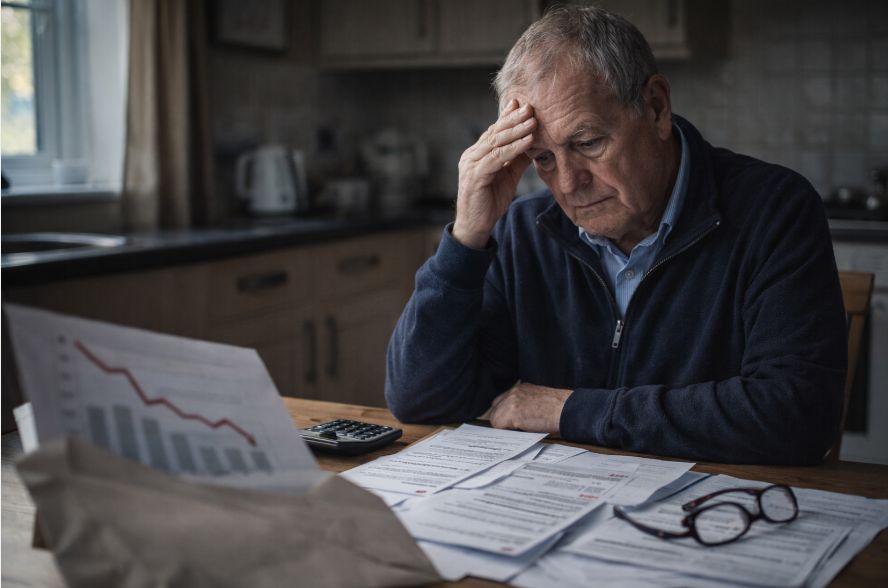

Imagine working for 40 years only to find your retirement fund vanishes in less than five.

This is not a hypothetical scenario it reflects a growing concern highlighted by Skipton Building Society in its April 2026 research. What many people across the UK consider a reasonable retirement cushion £100,000 is now being described as potentially inadequate for even a modest lifestyle.

This article explores the reality behind the “£100k pension myth,” explains how long savings may realistically last, and outlines practical steps to help individuals make more informed retirement decisions.

Why Is Skipton Building Society Warning About a £100k Pension?

The warning stems from a clear mismatch between expectations and financial reality.

The warning stems from a clear mismatch between expectations and financial reality.

A significant number of retirees believe that £100,000 will support their retirement comfortably. However, current economic conditions particularly inflation, rising living costs, and increased life expectancy mean that this figure may fall short much faster than expected.

Research shows that:

- One in seven people aged over 65 believe £100,000 is sufficient for their retirement

- A large portion of UK adults have not actively planned their retirement finances

- Some retirees are unaware of how much they are contributing or withdrawing

This gap between belief and reality is what prompted the warning.

How Long Will a £100k Pension Really Last in the UK?

In simple terms, a £100,000 pension pot may last approximately 4 to 5 years under a moderate standard of living.

This estimate assumes:

- Annual spending of around £25,000

- Access to the full State Pension

- No major unexpected financial shocks

While this may vary based on lifestyle and personal circumstances, the broader takeaway remains consistent: the duration is shorter than many expect.

What Does a “Moderate” Retirement Lifestyle Actually Cost?

A moderate retirement lifestyle in the UK typically includes:

- Essential living costs such as housing, utilities, and food

- Basic leisure activities like occasional dining out or holidays

- Transport and healthcare expenses

These combined costs can easily reach or exceed £25,000 per year, especially in today’s economic environment.

Even careful budgeting may not significantly extend a £100,000 pension beyond a few years if these costs are maintained.

Why Do Many People Still Believe £100k Is Enough?

Several factors contribute to this belief:

Several factors contribute to this belief:

- Outdated benchmarks from previous decades

- Underestimation of inflation and rising costs

- Overreliance on the State Pension

- Lack of regular financial review

In many cases, individuals form expectations early in their careers and fail to adjust them as economic conditions evolve.

What Happens If Your Pension Runs Out Too Early?

Running out of pension savings can have serious implications.

Many retirees in the UK are already facing this situation, leading to:

- A return to part-time or full-time work

- Reduced quality of life

- Increased financial stress during later years

Research suggests that one in six retirees has returned to work due to financial necessity. This highlights the importance of realistic planning.

How Does the State Pension Fit Into This Picture?

The State Pension plays an important role, but it is not designed to fully fund retirement.

It is intended to cover basic living costs, not a comfortable lifestyle. This means individuals relying heavily on it may still face a financial shortfall.

To qualify for the full State Pension, individuals must meet National Insurance contribution requirements. Gaps in contributions can further reduce income.

What Is the New Recommended Pension Target?

To achieve a more stable and comfortable retirement, a higher savings target is now being encouraged.

To achieve a more stable and comfortable retirement, a higher savings target is now being encouraged.

A pension pot of £200,000 or more is increasingly seen as a more realistic baseline for long-term sustainability.

This does not guarantee financial security, but it significantly improves the chances of maintaining a consistent lifestyle throughout retirement.

How Much Should You Be Saving Each Month?

The amount required depends heavily on when saving begins.

For a £100,000 target:

- Starting at age 30: around £89 per month

- Starting at age 40: around £168 per month

- Starting at age 50: around £375 per month

For a £200,000 target:

- Starting at age 30: around £175 per month

- Starting at age 40: around £330 per month

- Starting at age 50: around £740 per month

Starting earlier allows individuals to benefit from long-term growth and reduces the monthly financial burden.

How Does Pension Drawdown Strategy Affect How Long Your Savings Last?

Pension drawdown strategy plays a crucial role in determining whether a £100,000 pension lasts four years or significantly longer.

Many retirees withdraw funds without a structured plan, which increases the risk of depleting savings too quickly. A poorly managed drawdown approach can accelerate financial decline, especially during periods of inflation or market volatility.

A more sustainable approach involves:

- Withdrawing smaller, consistent amounts instead of large lump sums

- Adjusting withdrawals based on market performance

- Keeping a portion of the pension invested for continued growth

For example, withdrawing £25,000 annually from a £100,000 pot will exhaust it in roughly four years. However, reducing withdrawals and combining income sources could extend its lifespan.

This highlights an important principle:

It is not just how much you have but how you use it that determines financial longevity.

Could Lifestyle Adjustments Make a £100k Pension Last Longer?

Yes, lifestyle choices can significantly influence how long a pension lasts.

Yes, lifestyle choices can significantly influence how long a pension lasts.

While a £100,000 pension may not sustain a moderate lifestyle for long, adjusting spending habits can extend its usability.

Common adjustments include:

- Downsizing housing to reduce living costs

- Limiting discretionary spending such as travel or luxury purchases

- Taking advantage of senior discounts and benefits

- Reducing energy usage and household expenses

However, it is important to recognise the trade-off. Lower spending may extend financial resources, but it can also impact overall quality of life.

A balanced approach is often the most effective maintaining essential comfort while identifying areas where costs can be reduced without major lifestyle sacrifices.

Ultimately, relying solely on lifestyle cuts is not a long-term solution. It works best when combined with:

- Increased savings before retirement

- Better financial planning

- Diversified income sources

How Does Inflation Impact Pension Savings Over Time?

Inflation gradually reduces the purchasing power of money.

Even modest inflation rates can significantly impact retirement savings over 20 to 30 years. What feels like a comfortable amount today may not hold the same value in the future.

This is one of the key reasons why fixed pension targets can quickly become outdated.

Are Younger Generations Taking Retirement Seriously?

Younger generations show mixed behaviour when it comes to retirement planning.

Many have not yet actively considered retirement, while others expect to need significantly larger pension pots often exceeding £1 million.

This reflects growing awareness of rising costs, but also highlights a delay in taking practical action.

Why Are Some Retirees Returning to Work?

Returning to work after retirement is becoming increasingly common.

This is often driven by:

- Insufficient pension savings

- Rising living costs

- Longer life expectancy

For some, it is a choice to stay active. For others, it is a financial necessity.

What Practical Steps Can Help Your Pension Last Longer?

There are several effective ways to improve pension sustainability:

There are several effective ways to improve pension sustainability:

- Review pension contributions regularly

- Increase savings where possible

- Delay retirement if financially viable

- Use structured withdrawal strategies instead of large lump sums

- Monitor spending habits during retirement

Even small adjustments can make a meaningful difference over time.

How Can You Check If You Are on Track for Retirement?

Assessing pension readiness is a crucial step.

This can include:

- Reviewing current pension balances

- Estimating future retirement income

- Checking State Pension eligibility

- Using pension calculators or financial planning tools

Regular reviews help ensure that financial plans remain aligned with changing circumstances.

What Is the Biggest Mistake People Make With Pensions?

One of the most common mistakes is delaying action.

Many individuals assume they have more time than they actually do. Others rely on outdated assumptions or avoid reviewing their finances altogether.

Without proactive planning, small gaps can turn into significant shortfalls over time.

How Can You Avoid the “£100k Pension Trap”?

Avoiding this situation requires a shift in mindset.

Rather than focusing on a single savings figure, individuals should:

- Plan based on expected retirement duration

- Account for inflation and lifestyle changes

- Build flexibility into their financial strategy

A dynamic approach to retirement planning is far more effective than relying on fixed targets.

What Should You Do Next to Secure Your Retirement?

Taking action early is the most effective way to improve outcomes.

Steps to consider include:

- Reviewing current pension contributions

- Increasing savings where possible

- Seeking financial guidance if needed

- Staying informed about changes in pension policies

These actions can help create a more stable and predictable financial future.

Conclusion

The Skipton Building Society pension warning serves as an important reminder rather than a cause for alarm.

It highlights how quickly financial assumptions can become outdated and emphasises the need for ongoing planning. While a £100,000 pension pot may no longer provide long-term security, there are still clear and practical ways to improve retirement outcomes.

The key message is straightforward: informed decisions made today can significantly influence financial stability in later life.

FAQs About Skipton Building Society Pension Warning

How accurate is the estimate that £100k lasts only 4 years?

It is a general estimate based on moderate annual spending. Actual outcomes vary depending on lifestyle and financial management.

Can a smaller pension still work with careful planning?

Yes, but it often requires reduced spending, additional income sources, or later retirement.

What role does private pension investment play?

Private pensions can help grow savings over time, especially when combined with consistent contributions.

Should people delay retirement if savings are low?

In some cases, delaying retirement can improve financial stability by allowing more time to save.

How often should pension plans be reviewed?

Ideally, pension plans should be reviewed annually or after major life or economic changes.

Is it too late to improve pension savings after 50?

It is never too late, but contributions may need to be higher to achieve meaningful results.

Are financial advisors necessary for retirement planning?

They are not essential, but they can provide valuable guidance, especially for complex financial situations.